Harsh Municipal Bond Ratings

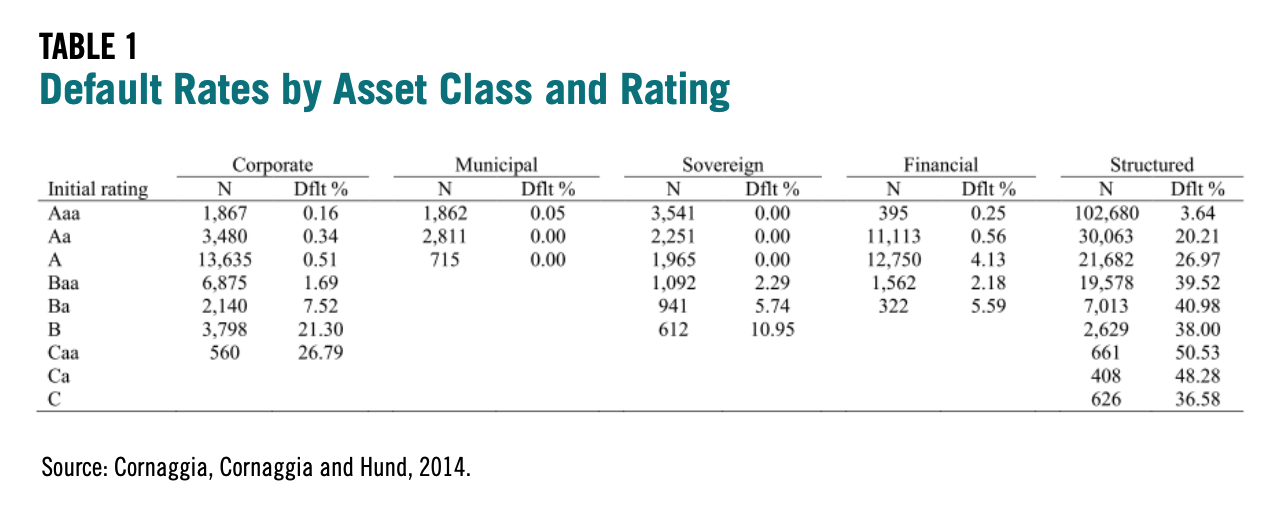

CORNAGGIA, CORNAGGIA, AND HUND1 evaluated default rates by major asset class by Moody’s rating. Their results are reproduced in Table 1.

High default percentages for Aaa and Aa bonds suggest more lenient rating standards. Overall, the authors find that government bond issuers (sovereign and municipal) are rated more harshly than corporate issuers—including financial corporations—which are rated more harshly than structured finance securities. They further observe that rating severity is inversely proportional to rating fee levels. Rating agencies charge structured finance issuers the most and government bond issuers the least, with corporates in between.

These findings are corroborated by Micah Hauptman and Barbara Roper in a March 2014 Securities and Exchange Commission (SEC) comment letter.2 The authors reviewed forms Nationally Recognized Statistical Ratings Organization (NRSRO) filed by Moody’s, Standard & Poor’s and Fitch, observing large differences in default and downgrade behavior across asset classes. The authors conclude:

Ratings agencies are likely to grant more favorable ratings to issuers who are likely to seek significant current and future business. This phenomenon is likely reinforced when there are few issuers in a certain asset class, which is common in the structured finance arena, because those issuers will choose whichever NRSRO rates their securities most favorably, and because NRSROs won’t risk losing any business from an issuer with such market power. (Page 25)

Since the municipal bond market is fragmented among tens of thousands of relatively small issuers, a local government has far less ability to affect rating agency behavior than Goldman Sachs, JP Morgan and other major financial industry players that create structured finance instruments.

Within the broad category of government bond issuers, US states have performed exceptionally well. In fact, the last time any state entered default status was 1933, when both Arkansas and Louisiana missed interest payments. Louisiana’s problem—the result of a local bank failure—was quickly rectified. Arkansas did not fully emerge from default until 1941, when the Reconstruction Finance Corporation—a federal agency—purchased previously non-performing Arkansas bonds at par (meaning that private bondholders experienced no loss of principal).3

Thus, US states have reliably serviced their bonds for as long as most anyone can remember. Yet most of their obligations do not receive the highest ratings from the major rating agencies. For example, rating histories published by the California State Treasurer4 show that all three major rating agencies have rated California below AAA/Aaa5 since the early 1990s.

Moody’s6 downgraded California from Aaa to Aa1 in February 1992. Since then, the state’s rating has fallen as low as Baa1, which is seven notches below Moody’s highest rating. Currently, Moody’s assigns California a rating of Aa3, three notches below Aaa. Two states—Illinois and New Jersey—currently have lower ratings than California: A3 and A1 respectively.

In 2008 Congressional testimony7 , Moody’s Senior Managing Director Laura Levenstein stated:

Investors in corporate or structured securities typically have looked to Moody’s ratings for an opinion on whether a security or an issuer will meet its payment obligations. Historically, this type of analysis has not been as helpful to municipal investors. If municipal bonds were rated using my global ratings system, the great majority of my ratings likely would fall between just two rating categories: Aaa and Aa. This would eliminate the primary value that municipal investors have historically sought from ratings—namely, the ability to differentiate among various municipal securities. I have been told by investors that eliminating that differentiation would make the market less transparent, more opaque, and presumably, less efficient both for investors and issuers (Page 122).

Levenstein asserts that Moody’s provided the harsher rating scale for municipal bonds because of investor demand. But I wonder whether Moody’s surveyed a good cross-section of municipal bond investors, which include large numbers of individuals—who rarely have any reason to contact a rating agency and who were probably unaware that rating agencies have separate standards for municipal bonds. Most likely, the universe of investors Levenstein and her colleagues consulted included a disproportionate number of bond insurers, who had a vested interest in perpetuating inconsistent rating methodologies—as discussed below.

If rating agencies were primarily concerned with providing greater differentiation among municipal bonds, they could have used a different set of symbols for these securities. They could have even assigned governments a fiscal score on a 0–100 scale.8 Joseph Pimbley notes that rating agencies already use different scales for short term debt and preferred stocks.9 Pimbley continues:

Had the CRAs truly wished to rate municipal bonds with different meanings for the ratings, they would have created rating scales with distinct symbols and explained them clearly. A good faith attempt to explain to investors, issuers, regulators and other stakeholders that municipal and corporate ratings are entirely dissimilar and incomparable would have required at the very least the imposition of distinct rating symbols (Pages 7–8).

- 1Jess Cornaggia, Kimberley J. Cornaggia and John E. Hund. Credit ratings across asset classes. Working Paper on Social Science Research Network, June 14, 2014. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1909091

- 2Consumer Federation of America comment letter regarding Request for Re-Proposal Relating to Nationally Recognized Statistical Rating Organizations. Micah Hauptman and Barbara Roper. March 3, 2014. https://www.sec.gov/comments/s7-18-11/s71811-78.pdf

- 3The Arkansas and Louisiana defaults are discussed in Jerome S. Fons, Thomas Randazzo and Marc D, Joffe, An Analysis of Historical Municipal Bond Defaults, Kroll Bond Rating Agency, November 14, 2011 (available with registration at https://www.krollbondratings.com/show_report/44)..

- 4California State Treasurer, Public Finance Division, History of California’s General Obligation Bond Ratings. http://www.treasurer.ca.gov/ratings/history.asp.

- 5S&P and Fitch use a ratings scale that ranges from AAA to D; Moody’s ratings range from Aaa to C. The highest ratings on the S&P/Fitch scale are: AAA, AA+, AA, AA-, A+, A, A-, BBB+, BBB and BBB-. The highest ratings on the Moody’s scale are Aaa, Aa1, Aa2, Aa3, A1, A2, A3, Baa1, Baa2 and Baa3.

- 6Most of the narrative below focuses on Moody’s ratings, since it is the oldest rating agency and has very comprehensive coverage. During the early 21st Century, rating agency behavior toward municipal and bond insurance issuers was similar.

- 7Municipal Bond Turmoil: Impact on Cities, Towns, and States. Hearing before the Committee on Financial Services, U.S. House of Representatives, 110th Congress, Second Session, March 12, 2008, Serial Number 110–99. Laura Levenstein’s testimony is available as a separate PDF file at http://archives.financialservices.house.gov/hearing110/levenstein031208….

- 8Such a scale is used for corporate borrowers by Rapid Ratings International, a non-NRSRO rating firm. http://www.rapidratings.com/company/

- 9Declaration of Joseph Pimbley In Support Of Plaintiffs’ Anti-Slapp (C.C.P. §425.16) Prong Two Showing, Ambac Bond Insurance Cases, Superior Court of California Case Number CJC-08- 004555.