Arguments Against

The movement of GASB in recent years, through Statements 67 and 68, have been in precisely the opposite direction to the arguments presented here. The arguments against the perspective presented here are thus well known, and worth airing and addressing.

Facing facts: On not kicking the can down the road

“The problems that we have right now were caused in the largest part by delaying payments, kicking the can down the road,” said Sen. Daniel Biss, D-Evanston, a key pension negotiator. “It’s very dangerous. It should only be done if it’s paired with a very specific, clear plan for how all the payments will be made and the pension systems will be brought back to full payment.”70

In debates over pension funding, proponents of austerity, in favor of paying off the unfunded liability as quickly as possible will often accuse their opponents of simply wanting to “kick the can down the road” and avoid facing the hard truths. The Chicago Tribune article quoted above even uses the phrase in a sub-head. The argument made is that these problems must be addressed eventually so therefore a hard-nosed look at the facts will support addressing them now. People who suggest otherwise are irresponsible procrastinators who will eventually be forced to face the facts.

The metaphor itself is interesting, because kicking the can down the road is only a problem if there comes a point at which one can kick that can no further. As we saw above, under the right conditions, a pension system can pay benefits indefinitely at funding levels much lower than “full” funding. In other words, unless the combination of funding level and demographics creates a liquidity crisis, there is always room to “kick the can” further, and the metaphor misleads rather than enlightens. Obviously a system must be managed so as not to create a liquidity crisis, but this need not be done through 100 percent funding, as thousands of technically underfunded pension systems demonstrate each year.

It is true, however, that since the assumed rate of return in most systems is, at least in 2016, higher than the combination of inflation and economic growth, there is an advantage to putting money into the system sooner. One hundred dollars deposited now in an investment earning 7.5 percent interest will very likely be worth more ten years hence than one hundred dollars compounding at 3 percent inflation plus 2 percent economic growth. But the simple fact of this advantage does not then imply that all dollars not invested this way are wasted. Schools must be staffed and roads maintained; a government’s many commitments, opportunities, and responsibilities must be weighed against one another. Furthermore, many government expenses, such as infrastructure, public health, and education, can usefully be considered to be investments. Some of them will pay off at rates higher than a pension fund’s assumed rate of return. Even maintenance costs for some assets can be considered to be investments that pay off handsomely.71 There are few governments where one expense can be allowed to trump all others.

Budgeting: Full funding reduces volatility

Another reason to value full funding is the consistency of employer payments. In a fully-funded system, when investment returns vary, the resulting variation in necessary premiums (from employees or employer) is usually small enough to be unimportant. Because the payments into the system are larger, a partially funded system will see correspondingly larger variation in the required premiums from the same investment variations. Volatility is an important concern in public finance. Because the budgeting process is cumbersome, dramatic changes in expenses tend to become controversial, no matter their relative size.

As true as this is, one way to amplify the volatility of a partially funded system is to amortize the unfunded liability on a fixed schedule. As the fund progresses down the road to amortization, the effects of variation in investment returns become ever more extreme.

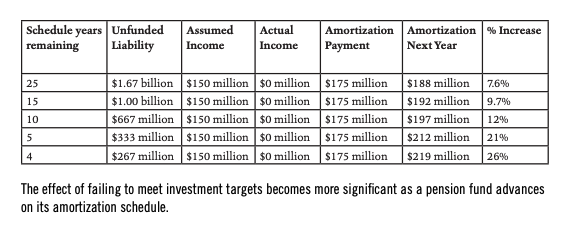

A plan with $4 billion of liabilities, funded at only 50 percent, is probably assuming a return of about $150 million in investment income, if it uses a typical 7.5 percent rate. Assume that, in one year, contributions to the system include $175 million devoted to paying down the unfunded liability on year five of a 30-year course. If investment returns fall $150 million short that year, so there is no investment income, there will be little progress on the unfunded liability, as most of the contributions must go to fund the pension checks. As a result, the unfunded liability will remain the same, and there will be one less year in which to amortize the same debt, by raising the required payment for the next year. (See table on page 27.)

After such a shortfall, in order to stay on schedule to pay off the debt, the following year’s amortization payment will have to be $188 million, an increase of 9 percent. This may not seem tragic, but if the government had been on year 20 of the same amortization schedule, suffering the same loss would cause a 12 percent payment increase the next year. Were it on year 25, with only 5 years to go before achieving full funding, the required increase in the amortization payment would be 21 percent. On year 26, the increase would be 26 percent, ramping up dramatically as the remaining time in the schedule declines. This is true for a pension fund that has stayed exactly on track on its amortization schedule until then. For a pension fund that has fallen behind at all, the increases at the end will be much larger, as the amortization of losses accumulates. Large increases will frequently be deemed politically infeasible and so many amortizations will not be completed successfully.

In the author’s experience, amortization schedules developed under these rules tend to seem reasonable only at the outset. A few years in, after being exposed to the vagaries of real-world investments, they usually call for utterly unmanageable increases in amortization payments at the very end of the schedule, often just in the last three or four years. This is an unremarkable outcome of the arithmetic of the reductions in the amortization period. The only remarkable part about it is when the government in question decides to “buckle down” and try harder rather than simply relax and restart the amortization schedule.

In other words, full funding is a worthy goal to prevent volatility in payments. But if, in order to prevent a problem one has to endure it—in an amplified form—sensible people might be led to question the therapy.

A better way to amortize shortfalls due to volatility is to amortize them on the same time scale as the system amortization. If a shortfall occurs in year 20 of a 30-year schedule, that shortfall is amortized over 30 years rather than the remaining 10. This will unavoidably make the amortization much longer, but 30 years is an arbitrary choice for a system being managed in perpetuity. Some pension systems (e.g. the State of Rhode Island employee pension system) have adopted this method of accounting, but it is far from universal.

Accounting clarity: What questions can you answer?

Accounting systems are designed to make clearly available the answers to the important questions one might ask about some enterprise. A business, for example, must be able to track whether it is earning a profit. Accrual accounting was invented to make clear whether a business is solvent, or even profitable. It does not, however, give a very good picture of the cash position for a business. This is less important for a company that might make its routine purchases with a line of credit, for example, so accrual accounting is used in most businesses.

An entirely different set of considerations obtain for a typical household, which is usually more interested in simply not experiencing a liquidity crisis. For a household, cash accounting is more useful in a day-to-day sense, even if it does not give a perfect picture of a household’s solvency. The appropriate accounting system depends heavily on the important questions, and the context in which they are asked.

For a pension system, the question of solvency in perpetuity is the important question. It is vital to know whether a system will receive the assets it needs to pay the liabilities it owes, out into the indefinite future. By making the standards uniform, and closing some reporting loopholes, GASB 68 makes answering important questions about the funding situation of a particular plan simpler and easier.

Unfortunately, the questions this system answers are not the most pertinent. That is, the GASB rules do a good job of answering, “How much money will this plan need to pay off its debts if it is closed tomorrow?” But most plans are not going to be closed tomorrow, so this is usually not very useful information. A more useful question might be along the lines of “How are we doing?” or “How much volatility will we suffer as we go along paying our bills?” The GASB rules provide those answers only in an oblique manner, for those willing to read past the headline numbers, just as a household’s solvency must be ascertained by looking beyond their bank balance.

In other words, the clarity provided by the GASB rules comes at the expense of making the situation seem much more dire than necessary. By ignoring, if not actually undermining, the value of the collective strength of a pension plan, the rules do a deep disservice to those who have contributed loyally to the plans for decades. The new rules will also require governments to add a deficit of billions of dollars to their governments’ bottom line, something few political leaders have the will to ignore.

As of this writing, governments across the country have only just begun to comply with the new rules, and as yet, no one really knows whether the bond-rating agencies will overreact or ignore the colossal new debts that are appearing on municipal bottom lines. Either way, it is not at all certain that clarity has been added to the situation.

- 70Hal Dardick and Monique Garcia. “Emanuel’s pension plan: Relief on payments, casino to pay for it.” In: Chicago Tribune (May 2015). 6/21/15. URL: http://www.chicagotribune.com/news/ct-chicagopension-payment-law-0527-2….

- 71See, for example, Wei Lin Koo and Tracy Van Hoy, of Jones Lang Lasalle, a large Chicago real estate firm, who developed estimates for the return on investment for preventive maintenance of various real estate assets such as HVAC equipment. Their estimates are that simple maintenance expenses can be construed as investments whose return is over 500%: Determining the Economic Value of Preventive Maintenance, 6/24/16 http://www.pmmi.org/files/ms/certified/newsletters/preventivemaintenanc…