An Alternative Model

I PROPOSE A MODEL under which municipal bond issuers are rated in an automated fashion based on economic and accounting metrics. Below I sketch out a model that can be applied to US general purpose local governments, such as cities and counties. The proposed model provides higher ratings overall, but still would have assigned relatively poor ratings to defaulting cities such as Detroit, Harrisburg, Scranton, San Bernardino and Stockton. This model is not intended to be a final product, but rather a concrete example of what is possible. I encourage other researchers to offer refinements or alternatives to the approach outlined here.

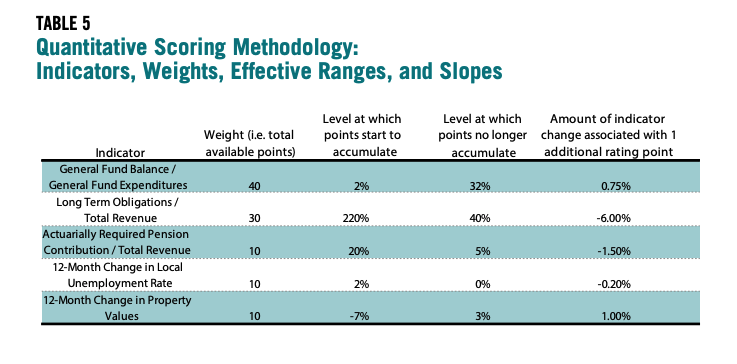

The model relies on five indicators, including three accounting ratios and two economic indicators. The intuition behind the model is that bankruptcy and default are triggered by some combination of insufficient general fund balance, excessive indebtedness (and other long term obligations), and negative revenue trends. In previous research, I have found general fund balance to be the strongest predictor; consequently, it receives the highest weight in the model. The model considers both long term obligations on the balance sheet plus a measure of pension burdens to incorporate indebtedness (these measures can be consolidated once GASB 68 is implemented, since this new standard will require governments to report future pension costs as a liability). Revenue trend is captured by two economic indicators: change in housing prices and change in unemployment rate. The housing price component offers a leading indicator of property tax collections.

To support comparability across jurisdictions of varying sizes, the model uses accounting ratios rather than single values. In the case of general fund balance, the amount is divided by general fund expenditures. The quotient can be intuited as the amount of time the general fund balance would last (as a percentage of one year) if no new revenues were collected.

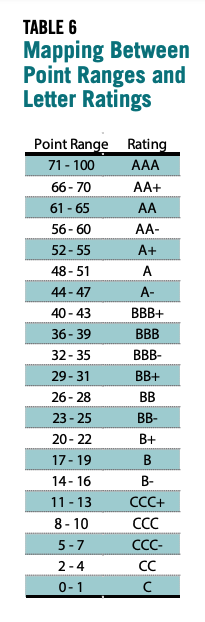

Indicator levels are translated into “rating points.” The maximum number of rating points a local government can receive is 100; the minimum possible score is 0. Point ranges are associated with letter ratings, so the assignment of a letter grade is a simple table lookup. An agency using this system can publish each entity’s point score in addition to its rating to provide users with greater granularity.

The conversion of an indicator value to a score requires some explanation. This description uses the general fund balance indicator as an example. Under the model points only accumulate within a relevant range. In the case of the general fund balance to expenditure ratio, that range is 2 percent to 32 percent. Any ratio level below 2 percent is associated with 0 points and any ratio level above 32 percent is associated with 40 points—representing the 40 percent weight assigned to this indicator. As the ratio rises from 2 percent to 32 percent, points are assigned on a straight line basis. Each increase of 0.75 percent in the ratio is associated with an extra point. Thus a ratio of 2.75 percent translates to 1 point, 3.50 percent translates to 2 points, 4.25 percent translates to 3 points, etc.

These caps and floors roughly capture the declining marginal importance of an indicator once it moves outside a relevant range. A city with a 101 percent general fund balance ratio is not meaningfully safer than a city with a 100 percent ratio. Both cities have plenty of liquid, discretionary assets available to meet their obligations.

Table 5 shows the indicators included in the rating model. Table 6 shows the total point ranges associated with particular letter ratings